The Law of Supply and Demand: What Is It?

Two fundamental economic theories are combined in the law of supply and demand to explain how changes in the price of a resource, good, or service impact its supply and demand.

Supply grows as the price rises, but demand drops. In contrast, as the price falls, supply is constrained and demand is increased.

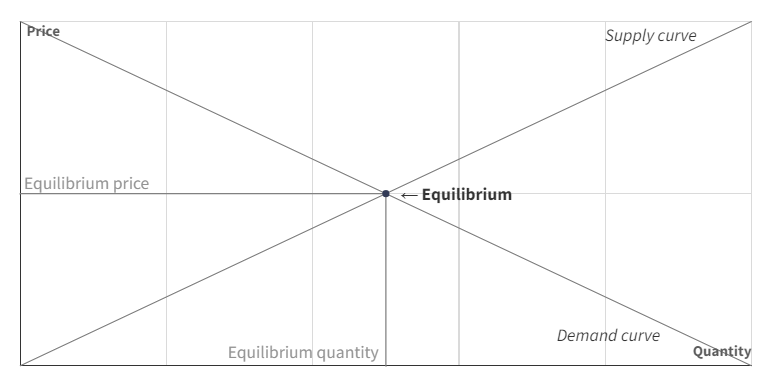

On a graph, levels of supply and demand for various prices can be represented as curves. The intersection of these curves denotes the point at which the market is said to have reached its equilibrium, or market clearing price, and symbolizes the process of price discovery in the market.

MAIN TAKEAWAYS

- According to the law of demand, demand for a good or resource will decrease as its price increases and increase as its price decreases.

- According to the law of supply, on the other hand, higher prices tend to increase an economic good’s supply while lower ones tend to reduce it.

- The intersection of the supply and demand curves, which balances supply and demand, is a graphic representation of the market-clearing price.

- The product’s price elasticity refers to the extent to which changes in price translate into changes in demand and supply. The demand for needs is comparatively inelastic, meaning that it responds less quickly to price changes.

Understanding the Law of Supply and Demand

It may seem obvious that in any sale transaction, the price satisfies both the buyer and the seller, matching supply with demand. The interactions between supply, demand and price in a (more or less) free marketplace have been observed for thousands of years.

Several historical thinkers saw a distinction between a “fair” price based on costs and equitable returns and one at which the sale was actually conducted, much like modern critics of market pricing for some commodities

The work of Enlightenment economists who investigated and described the link is the foundation of our knowledge of price as a signaling mechanism balancing supply and demand.

It’s important to note that supply and demand may not always react to price changes correspondingly. Price elasticity describes how much a product’s demand or supply is impacted by price fluctuations. Demand variations for products with a high price elasticity of demand will be more pronounced. Contrarily, because people can’t live without them easily, the price of needs will be relatively inelastic, which means that demand will fluctuate less in response to price fluctuations.

Price discovery based on supply and demand curves assumes a market where buyers and sellers are free to transact or not, depending on the price. Taxes and regulations, supplier market power, the presence of substitute goods, and economic cycles are only a few examples of the variables that might change the shape or location of supply or demand curves. Nonetheless, the commodities impacted by these external influences continue to be susceptible to the basic principles of supply and demand as long as buyers and sellers have agency. Let’s now think about how supply and demand react to price changes in turn.

Law of Demand

The law of demand states that all other things being equal, demand for a commodity changes inversely to its price. In other words, the level of demand decreases as the price increases.

Because consumers’ spending power is constrained due to their restricted resources, demand for a given good or service declines as prices rise. In contrast, as the product becomes more affordable, demand increases.

Demand curves consequently slope downward from left to right, as shown in the graph below. The income impact describes changes in demand levels as a result of a product’s price in relation to consumers’ resources or income.

There are, of course, exceptions. One is Giffen goods, which are commonly inexpensive essentials also referred to as subpar goods. When incomes increase, demand for inferior goods declines as people switch to higher-quality options. Yet, the substitution effect causes a product to become a Giffen good when its price increases and its demand increases as a result of consumers using more of it in place of more expensive alternatives.

Veblen goods, which are luxury items that appreciate in value and thus produce higher demand levels as their prices grow since the price of these luxury products signifies (and possibly even increases) the owner’s status, are at the other end of the income and wealth spectrum. Thorstein Veblen, an economist, and sociologist created the idea and came up with the term “conspicuous consumption” to characterize it. Veblen goods are named after him.

The Law of Supply

The amount supplied and price fluctuations for a product are related to the law of supply. The relationship between the law of supply and the law of demand is direct rather than inverse. The quantity offered increases as the price rises. All things being equal, decreased supply results in lower costs.

Prices that are higher encourage producers to produce more of the good or commodity, given that their costs aren’t rising as quickly. A cost squeeze brought on by lower pricing restricts supply. Supply slopes are as a result upwardly sloping from left to right.

Similar to how supply restrictions can affect demand, supply shocks can result in a disproportionate price change for a commodity that is necessary for production.

Law of Supply and Demand

Equilibrium price

The price at which supply and demand balance creates a market equilibrium that is agreeable to buyers and sellers is known as the equilibrium price, also known as a market-clearing price.

Supply and demand in terms of the quantity of the commodities are balanced at the point where an upwardly sloping supply curve and a downwardly sloping demand curve intersect, leaving neither a surplus supply nor an unmet demand. The position and shape of the corresponding supply and demand curves, which are impacted by a variety of circumstances, determine the level of the market-clearing price.

Factors Influencing Supply

When product prices are below manufacturing costs in businesses where suppliers are unwilling to lose money, supply tends to decline until it is zero.

The number of sellers, their combined production capacity, how readily it can be increased or decreased, and the competitive dynamics of the business will all affect price elasticity. Taxes and rules may also be important.

Factors Influencing Demand

Among the most significant factors influencing demand are consumer wealth, preferences, and readiness to switch from one product to another.

Since the marginal utility of commodities decreases as the amount owned rises, consumer choices will depend in part on a product’s market penetration. The first automobile has a greater impact on people’s lives than the fifth addition to the fleet, and the TV in the living room is more useful than the fourth for the garage.

THANKS FOR READING